" height="10px" id="XcmADpzdE" transform="translate(1 1)" width="10px"/></svg>)

" height="12px" id="RZsNoKQqh" width="12.075px"/></g></svg>)

What is decentralized lending?

DeFi, or decentralized finance, has its roots in traditional finance (TradFi) and adapts traditional products to a new paradigm. One of the most critical aspects of both TradFi and DeFi is lending. In DeFi, loans are facilitated through smart contracts on blockchain networks, allowing for decentralized and trustless lending.

How does decentralized lending differ from traditional lending?

Decentralized finance (DeFi) lending differs from traditional finance (TradFi) lending in several ways. These include:

Decentralization: The most fundamental difference is that DeFi lending is decentralized. Meaning there is no central authority or intermediary that controls the lending process. Instead, smart contracts on a blockchain network facilitate lending.

Transparency: DeFi lending is transparent, and all transactions are recorded on a public blockchain, making it easy for anyone to track and verify.

Accessibility: DeFi lending allows anyone with an internet connection to access lending and borrowing services, regardless of location or credit history.

Automation: Through smart contracts, decentralized lending is fully automated. Eliminating the need for intermediaries such as banks and loan officers, resulting in faster and cheaper transactions.

Liquidity: Commonly decentralized lending protocols are built on liquidity pools, which enable borrowers to take out loans using different assets as collateral, giving them more options and allowing liquidity providers to earn interest on their assets.

Censorship resistance: Decentralized lending is censorship-resistant. No one can block or freeze a transaction, which makes it more secure and reliable.

DeFI lending protocols break down into two categories: overcollateralized and undercollateralized. Several DeFi loans exist, each with unique characteristics and features.

These include:

Overcollateralized loans: These loans require the borrower to put up collateral, usually in the form of cryptocurrency, to borrow funds. The collateral is then locked up in a smart contract and can be liquidated if the borrower defaults on the loans.

Undercollateralized loans: These loans require less upfront collateral than the required loan amount. This lending relies on the borrower’s creditworthiness, which is determined through various methods such as credit assessments, reputation scores, and social collateral.

Each type of DeFi loan has its advantages and disadvantages, and traditional traders need to understand the different features and risks associated with each before joining the DeFi space. Here is a detailed look at these types of lending.

What is overcollaterized lending?

Overcollateralized lending is where the borrower must provide collateral in an amount that exceeds the required loan’s value. As the borrower must put up more assets as collateral than they are borrowing, a buffer is created for the lender in case the value of the collateral drops.

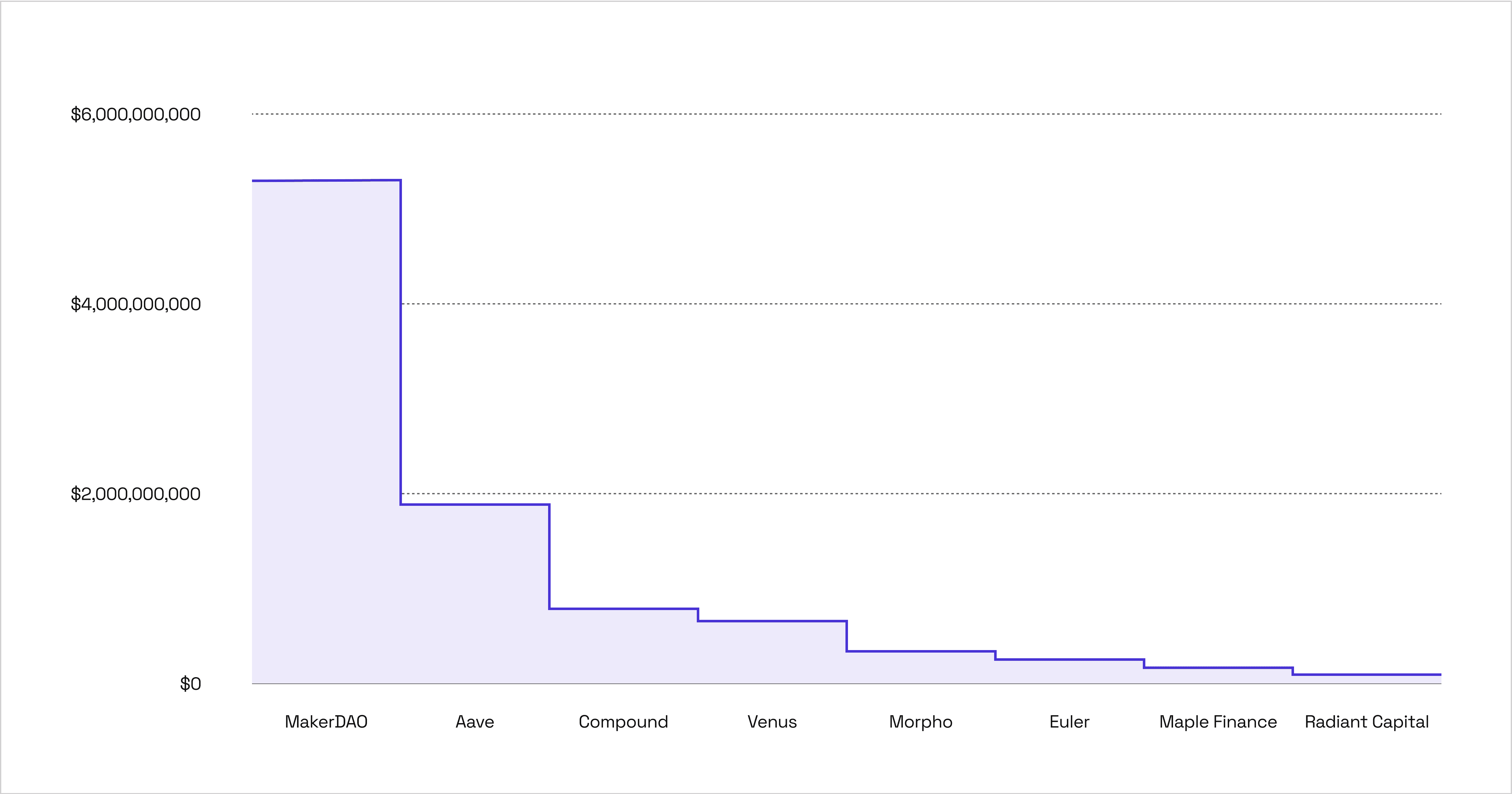

Collateralized lending takes an exceptional place in the DeFi ecosystem: TVL aggregated by those protocols is second only to DEXes, which is more than $12b. Several other popular overcollateralized lending protocols take a significant market share:

Top 10 Lending Protocols (Borrowing Volume, $)

MakerDAO: MakerDAO is a decentralized lending platform built on the Ethereum blockchain. It allows users to borrow DAI, a stablecoin pegged to the US dollar, by collateralizing Ether (ETH).

Aave: Aave is an open-source and non-custodial protocol for money market creation. It allows users to lend and borrow various assets, including cryptocurrencies, stablecoins, and tokens.

Compound: Compound is a decentralized lending platform built on the Ethereum blockchain that allows users to lend and borrow a wide variety of assets, including cryptocurrencies, stablecoins, and tokens. Compound acts as a crypto savings account — lenders can deposit their collateral on Compound and earn a variable interest rate on their assets.

How does overcollaterized DeFi lending work?

Decentralized finance overcollateralized lending works by allowing borrowers to deposit more collateral than the value of the loan they are taking out. This extra collateral acts as a safety cushion in case the value of the borrower’s collateral drops, allowing lower interest rates for the loan.

Here is a general overview of how overcollateralized DeFi lending works:

Borrowers deposit crypto assets as collateral into a smart contract.

The smart contract calculates the value of the collateral and sets a loan-to-value (LTV) ratio. For example, a 150% LTV ratio means the borrowers are depositing 1.5 times the value of the loan they are taking out.

At the same time, lenders deposit fiat currency (or stablecoins) into the protocol.

The smart contract automatically calculates and charges interest on the loan, manages the collateral, and enforces the loan terms.

If the value of the borrower’s collateral drops, the smart contract will automatically liquidate a portion of the collateral to cover the difference and maintain the LTV ratio.

Borrowers can repay the loan anytime, and the smart contract will automatically release the collateral to the lender it is fully repaid.

Once the borrower repays the loan, the lender receives these funds back with accrued interest.

Therefore, the whole process is entirely automated and secured by the smart contract. KYC or underwriting is unnecessary as each counterpart has zero knowledge of the other.

Overcollateralized DeFi: Pros and Cons

The key strength of these protocols is the decentralized nature of blockchain. In this type of lending, borrowers and lenders interact directly with each other without the need for intermediaries such as banks. Self-executing smart contracts fully facilitate the transactions, with all of the terms of the agreement directly written into their code. Other advantages worth knowing are:

Protection for lenders: Overcollateralization ensures that the lender can recover the loan’s total value even if the collateral’s value drops, reducing the risk of default for the lender.

Flexibility for borrowers: Overcollateralization allows borrowers to take out loans using a broader range of assets as collateral, giving the borrower more options and making it easier to secure a loan.

Liquidity provision: Overcollateralized lending protocols are often built on liquidity pools, which enable borrowers to take out loans using different assets as collateral while allowing the liquidity providers to earn interest on their assets.

Despite all of the advantages, the overcollateralized approach has its downsides. The major disadvantage of overcollateralized DeFi lending is capital inefficiency. The minimum collateralization ratios for volatile assets of 150% or more are typical for the money market and stablecoin protocols.

What is undercollateralized lending?

Undercollateralized lending is when the borrower puts up less collateral than the amount of required lending. Therefore, the lender is taking a greater risk, as the collateral does not fully protect them if the borrower defaults. A distant example of undercollateralized lending in TradFi is mezzanine financing: the company provides its shares as collateral to get debt financing from the bank.

Undercollateralized lending generally serves TradFi institutions to borrow directly from DeFi users instead of financial institutions or banks. The institution pays lenders back any outstanding principal or accrued interest when the loans mature. The borrower and DeFi protocol work together to establish terms for the line. Users can then assess the pool’s risk/reward tradeoff and choose to deposit their funds into the pool.

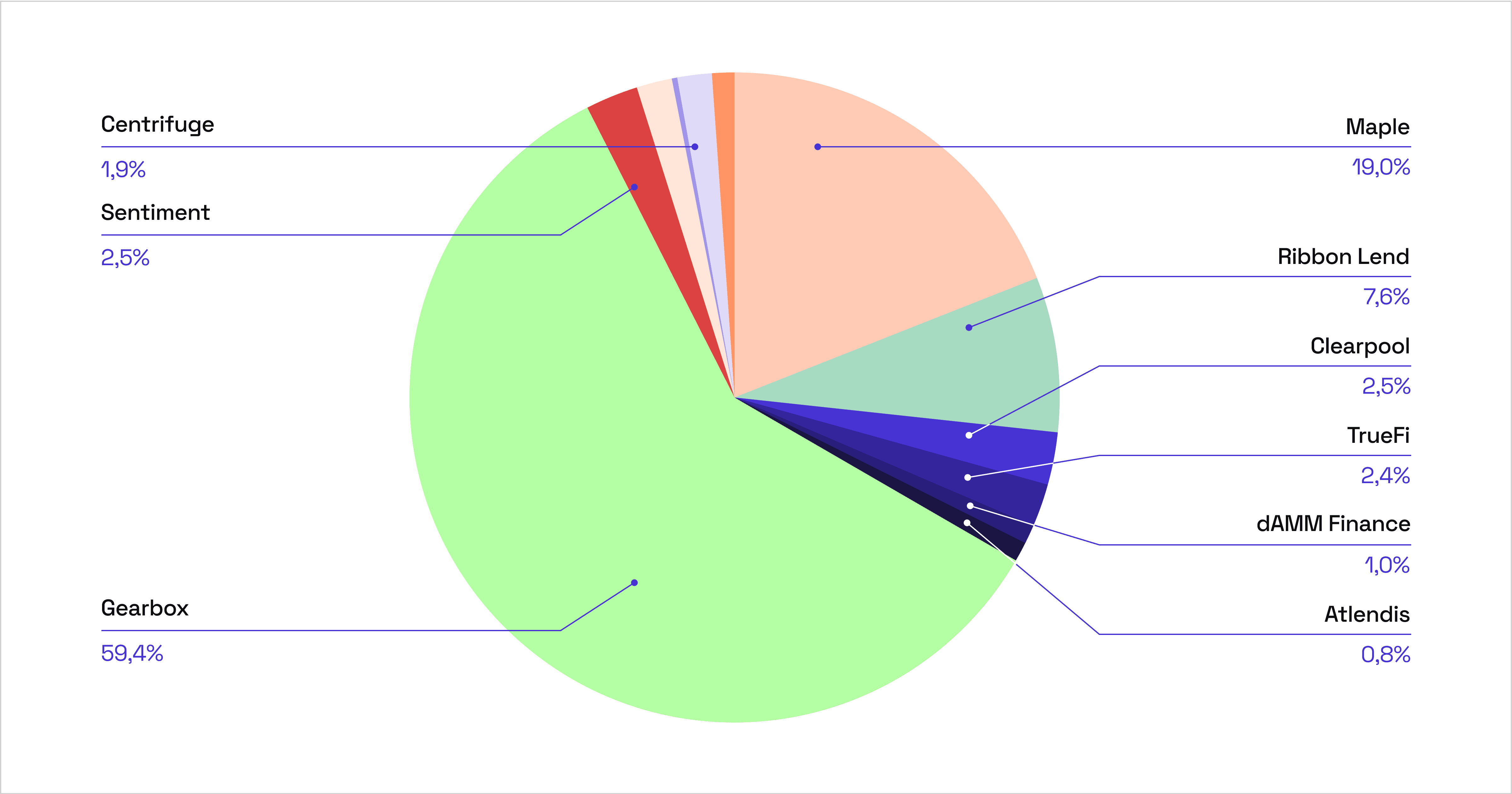

Uncollateralized Lending Protocols by TVL

The most popular platforms are Goldfinch, Maple Finance, and Gearbox. Together they hold a significant portion of the undercollateralized lending market with an outstanding loan balance of almost $300 million. Since undercollateralized lending is more specific, their market share is significantly less than overcollateralized ones.

How does undercollaterized DeFi lending work?

There are various methods for providing undercollateralized crypto loans, such as a tiered cash flow repayment structure or pooling lender funds, for greater portfolio diversity and reduced default risk. These approaches aim to meet the demand for undercollateralized loans in the traditional financial market. Some methods also include options for borrowers to undergo KYC/AML verification. Here are some of the most popular methods.

Gearbox and Sentiment

Gearbox and Sentiment focus on individual users and use immutable smart contracts.

Users must create an escrow wallet with the protocol to secure the loan. These wallets limit the user’s withdrawals to ensure the collateral always stays within the collateralization requirements. By only interacting with smart contracts explicitly approved by the protocols, they minimize the risk of bad debt. The protocols achieve this whitelist by using only the most established dApp.

This approach allows borrowers to use their capital more efficiently than overcollateralized ones. The minimum collateralization ratios for Gearbox and Sentiment are 10% and 20%, respectively. In other words, users can borrow with leverage of up to 10x (Gearbox) or 5x (Sentiment).

Although all operations happen on-chain, there are still risks associated with this approach. The whitelisted protocols used by Gearbox and Sentiment may be vulnerable to hacking. The result of hacking would be bad debt and loss of lender funds. Therefore, when evaluating their risk exposure, lenders must consider the potential smart contract and hack risk from all whitelisted protocols in addition to Gearbox or Sentiment.

Maple Finance, Goldfinch

These protocols offer institutional solutions for undercollateralized lending in DeFi. They use a trust-based loan model, similar to traditional financial LOC environments. Since these protocols are oriented towards TradFi players, it’s no wonder the model dominates the undercollateralized lending sector, comprising over 80% of its borrowing volume.

To borrow, potential borrowers need to go through a credit approval process, which varies depending on the protocol. To get approved, borrowers must undergo a risk assessment process by the lending platform or external auditors and analysts. Once the loan’s approved, an off-chain, legally binding agreement is formed between the borrower and the protocol. Making the approach not fully decentralized and heavily reliant on the off-chain processes.

The main risk in this category of undercollateralized lending is trust. As a lender, you must have faith that the entity you are lending to will repay the loan. It is vital to perform thorough due diligence before lending any significant amount and not blindly trust the borrower’s ability to repay the obligation. If the borrower becomes bankrupt, your claim to repayment is included with every other claim to the entity’s assets, and bankruptcy proceedings can be notoriously arduous and time-consuming, often taking years to settle.

dAMM

dAMM applies another approach. Historically, professional market makers had difficulties borrowing most of the crypto assets since DeFi undercollateralized lending primitives traditionally offered stablecoin-denominated loans. dAMM is trying to solve the problem of undercollateralized borrowing and lending markets for volatile assets.

Like other trust-based protocols, dAMM requires borrowers to undergo third-party due diligence before signing a legally-binding loan agreement.

The main feature of the protocol is the ability to reduce risk through diversification by aggregating lending supply and borrowing demand in different pools. With dAMM, borrowers can access any asset at an interest rate determined by the protocol’s algorithm. Meaning lenders are proportionally exposed to all parties borrowing their assets based on their utilization rate. By pooling together lending supply, lenders can benefit from diversification as the default or bankruptcy of one borrower would only affect a portion of the pool’s funds.

Like trust-based lending, lenders on dAMM face the risk of borrower default. However, spreading the risk among a diverse group of borrowers reduces the expected rate of loan write-offs, bringing it closer to the overall market default rate. However, aggregate lending on dAMM eliminates the ability for users to choose individual borrowers, increasing the reliance on credit assessments and the evaluation of borrower risk by third-party auditors. Also, the benefits of diversification can be limited if a single entity makes up a large portion of borrowing activity in a specific asset pool.

How does Arkis make DeFi lending more convenient?

Arkis Protocol is the core component of the Arkis platform. It includes smart contracts adapters for trading and liquidity pools and a multichain undercollateralized leverage feature powered by Arkis Margin Engine.

Arkis Margin engine calculates the initial and maintenance margin required to provide leverage to a user. It calculates risk on a portfolio level rather than individually. Meaning the short positions can offset the long positions. If the total portfolio risk is relatively low, the trader can get more leverage for these operations compared to having a single long or short position on different protocols.

Acting as the Prime Broker in its traditional meaning, Arkis Protocol allows users to access cross-chain leverage on various protocols with a lower loan-to-value ratio than traditional lending protocols.

About Arkis

Arkis — DeFi Prime Broker offers multichain, undercollateralized leverage powered by portfolio margin. Author Serhii Tyshchenko is the Co-founder and Chief Executive Officer.

You can follow us on LinkedIn and Twitter and join our Announcements channel on Telegram to be the first to hear about product updates.

You can apply by joining our exclusive allowlist to be the first to access Arkis. For updates straight to your inbox, join our biweekly newsletter.